Most Medicare Costs Are Increasing in 2024

Premiums, deductibles, and coinsurance amounts for Original Medicare generally change every year. Here’s a look at some of the costs that will apply in 2024.

Medicare Part A (Hospital Insurance) costs for 2024

- Premium for those who need to buy coverage: As much as $505 per month (down from $506 in 2023); however, most people don’t pay a premium for Medicare Part A

- Deductible for inpatient hospitalization: $1,632 per benefit period (up from $1,600 in 2023)

- Inpatient hospital coinsurance: $408 per day for days 61 through 90, and $816 per “lifetime reserve day” after day 90, up to a 60-day lifetime maximum (up from $400 and $800 in 2023)

- Skilled nursing facility coinsurance: $204 per day for days 21 through 100 for each benefit period (up from $200 in 2023)

Medicare Part B (Medical Insurance) costs for 2024

Monthly standard premium: Most people with Medicare who receive Social Security benefits will pay the standard monthly Part B premium of $174.70 in 2024, $9.80 higher than in 2023. This premium increase is mainly due to higher projected health-care spending.1

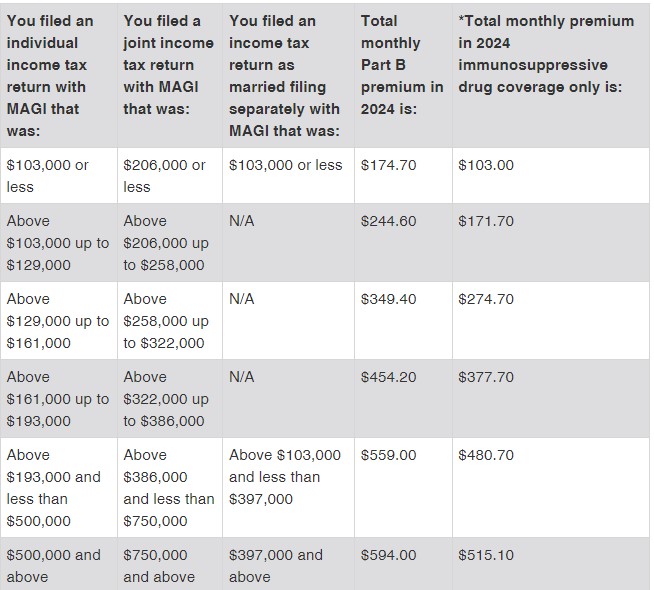

Premium for those with higher incomes: If your modified adjusted gross income (MAGI) as reported on your federal income tax return from two years ago (2022) is above a certain amount, you’ll pay the standard premium amount and an Income-Related Monthly Adjustment Amount (IRMAA), which is an extra charge added to your premium, as shown in the following chart.

*This premium applies to a benefit that extends coverage for immunosuppressive drugs for people whose full Medicare coverage ended 36 months after a kidney transplant and who do not have certain other types of health insurance.

People with higher incomes may also pay a higher premium for a Medicare Part D prescription drug plan, because an IRMAA will be added to the Part D basic premium based on the same income limits in the table above. Part D premiums vary, but the average basic monthly premium for 2024 is projected to be $34.50 (up from $32.09 in 2023). The average total premium for plans with enhanced coverage is projected to be $55.50 in 2024, down from $56.49 in 2023.

Annual deductible: People with Medicare Part B must also satisfy an annual deductible before Original Medicare starts to pay. For 2024, this deductible is $240 (up from $226 in 2023).

1) The Centers for Medicare & Medicaid Services, 2023

You can get more information on Medicare benefits in the Medicare & You 2024 Handbook at medicare.gov.

What about Medicare Part C premiums?

Medicare Part C (Medicare Advantage) costs vary by plan and some are premium-free, but the projected average premium for 2024 plans is $18.50 (up from $17.86 in 2023). If you have a Medicare Advantage plan, you will also have to pay the Medicare Part B premium.

To learn more about how we help at CapSouth, please visit our website at https://capsouthwm.com/what-we-do/

Prepared by Broadridge Advisor Solutions. © 2023 Broadridge Financial Services, Inc. CapSouth Partners, Inc, dba CapSouth Wealth Management, is an independent registered Investment Advisory firm. This material is from an unaffiliated, third-party and is used by permission. Any opinions expressed in the material are those of the author and/or contributors to the material; they are not necessarily the opinions of CapSouth. Information provided by sources deemed to be reliable. CapSouth does not guarantee the accuracy or completeness of the information. CapSouth does not offer tax, accounting or legal advice. Consult your tax or legal advisors for all issues that may have tax or legal consequences. This information has been prepared solely for informational purposes, is general in nature and is not intended as specific advice. Any performance data quoted represents past performance; past performance is no guarantee of future results.