We have held many 401(k) group meetings, one-on-one meetings, and phone calls with 401k participants this year. Understandably, participants are concerned with the markets and their 401(k) accounts. What follows are a couple of the common questions we’ve been asked and our general responses.

Question:

I am tired of contributing to my 401k and seeing it decline in value. Should I stop funding my 401k until the market stabilizes?

Answer:

We generally believe it best to continue contributing to your 401k to take advantage of dollar cost averaging. Contributing consistently is an important step in preparing for your retirement. You control your payroll deductions directly from your paycheck, helping to make this a simple and effortless process. Coupled with the principle of dollar cost averaging, this consistent payroll deducted contribution into your 401k throughout your working career can help you reach your retirement goals. Dollar cost averaging is the investment of equal amounts of money at standardized points over time, regardless of the price of the underlying securities. This can lower the impact of price volatility, as we are experiencing currently, and can lower the average cost of the investments being held.

Question:

My account has declined in value this year. Should I move my account into something safe (i.e., the money market, stable value, guaranteed account, or other cash equivalent) until I see the market rebound and I feel better about it?

Answer:

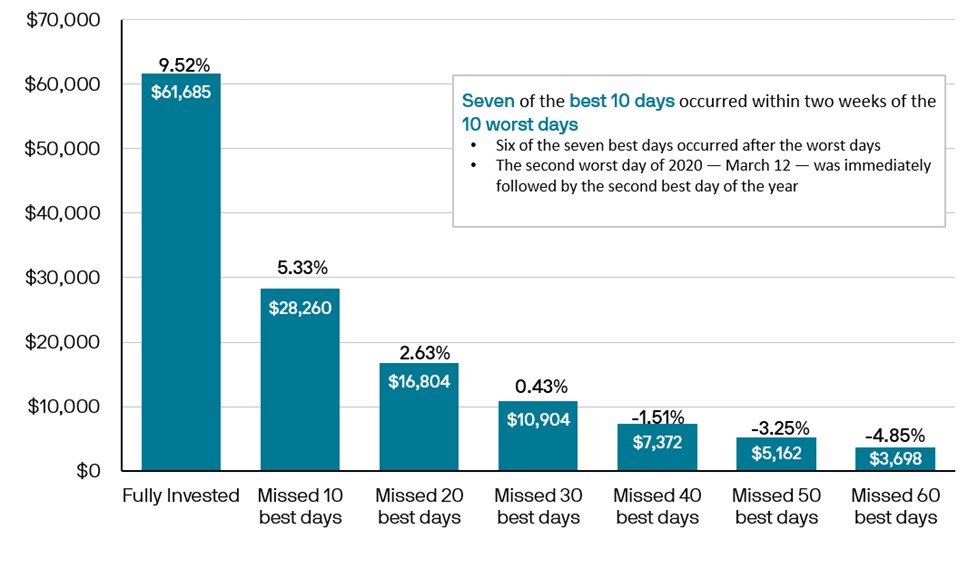

While everyone’s situation is different, we do not recommend trying to time the market; we believe it is better to focus instead on long-term investing. Timing the market includes when an investor moves some or all of their stock investments to cash in an attempt to avoid a market decline and with the hope of later reinvesting into a market rebound. While this sounds like a good strategy, this requires a participant to make two correct decisions: when to sell and when to buy. In the previous 12 bear markets of the S&P 500 Index, the index had positive returns a year following entering the bear market in all instances but three. The average one-year return was 23.9%. But reviewing each of these 12 bear markets individually on a one-month, three-month, six-month, and one-year basis, the returns they experienced differ significantly, making timing when to enter back into the market very difficult. (https://www.wsj.com/livecoverage/stock-market-today-dow-jones-bitcoin-fed-rates-06-14-2022/card/how-the-s-p-500-performs-after-closing-in-a-bear-market-yBwgfJwW8HGSNJaKg6LB).

It is very difficult to time when to leave the market to avoid market declines. It is equally as difficult to determine when to reinvest an account at the opportune time in order to experience any market rebound. We believe the best course of action is to maintain an appropriate, diversified mix of stocks and bonds, investing for the long-term in light of a dynamic plan for reaching your retirement goals.

In these difficult markets, we recommend holding fast to investment principles of resisting the urge to sell equities into declining markets, not attempting to time the market, focusing on investing with a long-term financial plan in mind, and continuing saving through dollar cost averaging. Do not hesitate to contact your CapSouth Financial Advisor to schedule a time to discuss your individual situation and to review your accounts.

CapSouth Partners, Inc, dba CapSouth Wealth Management, is an independent registered Investment Advisory firm. Any opinions expressed in the material are those of the author and are not presented as facts. Information provided by sources deemed to be reliable. CapSouth does not guarantee the accuracy or completeness of the information. CapSouth does not offer tax, accounting or legal advice. Consult your tax or legal advisors for all issues that may have tax or legal consequences. This information has been prepared solely for informational purposes, is general in nature and is not intended as specific advice. Any performance data quoted represents past performance; past performance is no guarantee of future results. The S&P 500 Index is an unmanaged, capitalization-weighted index that measures the performance of 500 large capitalization domestic stocks representing all major industries. Indices do not include fees or operating expenses and are not available for actual investment. This article contains links to third party content (content hosted on sites unaffiliated with CapSouth Partners). CapSouth makes no representations whatsoever regarding any third party content/sites that may be accessible directly or indirectly from this article. Linking to these third party sites in no way implies an endorsement or affiliation of any kind between CapSouth and any third party, including legal authorization to use any trademark, trade name, logo, or copyrighted materials belonging to either entity.

I’d like to address the elephant in the room. This year has been incredibly volatile for the stock market, and we’ve experienced some steep declines. It can be frustrating, confusing, and even frightening. Currently, we are in a bear market. Perhaps you have heard the term before and understand the feeling associated with a bear market but aren’t exactly sure what it is (besides scary). A bear market is when a market experiences a prolonged drop in investment prices. This is typically referenced when a broad market index falls by 20% or more from its recent high. There is tremendous noise in the media. Many investors are anxiously looking at account balances more frequently, particularly after experiencing a long run for the bull market. Experiences with past down-market events may be triggering strong feelings of concern. One of my greatest strengths is being able to stay calm in difficult situations and it serves me well as an Advisor. To help you tackle a difficult situation head on in hopes of instilling some calm in the chaos, I’ll discuss three things to consider in a bear market

Communication with your Advisor is Critical

I love talking to my clients. They share their dreams and lives with me. They trust me enough to delegate a large amount of their financial life to me. It’s very difficult to do my job well without clear and consistent communication from clients. It’s also difficult to plan for clients without truly understanding how they feel about risk, how they view money and even some of the personal biases they may have in their approach due to previous experiences. Some of my clients have never worked with an Advisor before working with me while others have unfortunately had very negative experiences working with an Advisor which is why they sought a change. For some, I serve as a sounding board and for others I offer trusted advice and guidance. The one unofficial role I never knew I would take on is counselor.

We often think of money as transactional. Most of our money exchanges are even labeled as transactions. We use labels such as “good” and “bad” to describe debt, investments, and even Advisors. We spend a great deal of time thinking about what we want to do with our money as well as thinking about what our money is doing in the markets. We don’t often talk about how we feel about money or our life experiences with money. This is ironic as the field of Behavioral Finance is growing. Research consistently indicates that client behavior is also a key indicator of financial success. One of the leading organizations in the financial planning industry, FPA, recently announced a new partnership to offer its members a Psychology of Financial Planning Specialist program. Covered in the program are topics such as Behavior Finance for Financial Planners, Counseling in Financial Planning Practice, and Implementing Financial Psychology into Practice. The industry has recognized what we as individuals may not be able to see right in front of us – dealing with money comes with a lot of emotion. It’s time we start talking about it.

While I believe communication is always important, communicating with your Advisor during a bear market about how you are feeling is crucial. A client recently shared that this was the first time they have ever felt uneasy. We had a long conversation about why they felt uneasy. We had reviewed the financial plan and were well in the confidence zone. There was plenty of cash to fund their needs for an extended period. We began to peel back the layers and have the hard conversations around emotions. Throughout the conversation I learned that when I said “everything is fine” the client perceived that as being dismissive. While that was never my intent, their honesty and vulnerability allowed me to clear the air and lean into even deeper conversation. I decided to ask the client a very tough question – are you uneasy because you have lost trust in me? Thankfully, they had not. After a while, they shared that they felt uneasy because it was the first time that they were experiencing a bear market while in retirement. It was scary to see the losses while on a fixed income. The client’s vulnerability in sharing those feelings took courage. We walked back through their financial plan, discussed “what ifs” and discussed how we might address them in the future. We didn’t abandon the plan and we didn’t make any sudden investment changes that were out of scope of the plan.

During this bear market, if you find yourself dealing with emotions that are new or ones you haven’t experienced in a while about your money, please tell your CapSouth Advisor. We truly care about you and we are here to listen. It is our responsibility to coach and guide you through the emotions so that we can limit behavioral influences. There is an adage that says, “the only people that get hurt on a roller coaster are the ones who jump off”. Advisors often use this to explain how behavioral changes impact money such as selling when the market is declining. We understand the emotions and we will spend the time needed to address concerns. Let us serve as the safety bar to keep you locked into the seat while we ride this roller coaster together.

Your Financial Plan Has a Long-Term Outlook

One of the things I love most about CapSouth is our dedication to Financial Planning. For most of my life, I only thought of a Financial Advisor as someone who manages money. My experience with them had been limited to those that work in the Broker world as an investment manager. Unfortunately, our industry has limited regulation on how the title Financial Advisor is used. I have had many new clients come to CapSouth with the same limited viewpoint. When I explain that we view investment management as a commodity and that our real value comes in planning, it can be a true mindset shift. Perhaps you had a similar experience when starting to work with us. We ask a lot of questions! We ask for a lot of information. For those that are just starting to work with us, it can be overwhelming although we do our best to make the onboarding process enjoyable. With all the information provided we then craft a financial plan and begin working with you to implement it. We review the financial plan every year in meetings and are consistently adjusting it because life happens. We start to focus more on the Confidence Score to answer the question “am I going to be, okay?”

Like the Wizard of Oz, I’m going to give you a peek behind the Advisor curtain. The Confidence Score is generated through a process called Monte Carlo simulation. So, what is it and why does it matter? Surprisingly, it’s not unique to the financial industry. It’s also used in physics and engineering. In our financial plans, we don’t have the certainty of knowing what the future holds. That includes knowing what the average rate of return will be for your plan. Therefore, the Monte Carlo simulation runs 1,000 trials of your plan using 1,000 different return possibilities to calculate the probability your plan will be successful. While you may not have considered worst case scenarios or bad returns, your financial plan already has.

When we dig into these simulations and look at the 1,000 Trials detail, we can get an even better understanding of the numbers. We can see year data in 5 year increments (Year 5, Year 10, etc.). We can also see End of Plan Dollars and The Year Your Money Goes to $0. These time frames are charted out by Trial Percentile. They include 1%, 25%, 50%, 75% and 99%. My personal plan has a Confidence Score at 88% (at time of writing this). When I look at these trials, I can see that in the very best scenario my plan would end with more money than my husband and I would know what to do with and would need a fantastic estate plan. I can also see that in the very worst scenario, we would run out of money in the year 2049. Does that scare me? Not at all. The reason? It’s an extremely unlikely scenario just like the one that looks amazing. The most realistic scenario is somewhere in between, and it’s why my Confidence Score is reassuring. (Friendly reminder here: This is not like school where the highest score is the best score. If my score is in the blue zone, it is considered an overfunded plan, and I need to ensure my estate plan is in order because I will likely be leaving money to heirs).

We don’t often get into these types of details in meetings because it can be data overload. The key takeaway right now during a bear market is that your financial plan is not surprised by a down market with negative returns. Neither is your Advisor. We take a long-range approach and understand that markets go down just like they go up. Historical charts show that the markets have always recovered. While history is not a predictor of the future, it does give us data to consider. While it can be difficult to zoom out when emotions are high it is important to remember the decisions made together with your Advisor when times were not as tumultuous.

It’s Not All Doom and Gloom

When we set the fear and frustration of a bear market aside for a moment, we can turn our focus to the bright spots in this market. No, I’m not talking about a “sweet deal” a friend is telling you about or even buying treasuries at 4%. I’m talking about the planning opportunities that present themselves during a bear market.

If you are still working or have cash on the sidelines, it’s an excellent opportunity to dollar-cost average new money into the market. If you are participating in a company retirement plan, it’s likely that you are already using this approach. Each time you contribute to your 401(k) you are investing new money. This may be weekly, bi-weekly, or twice a month depending on how your payroll is processed. It’s a great buying opportunity. I like to say we’re buying on sale and it’s an opportunity we haven’t had in a long time due to high market prices. We may only know that the bottom of the market has occurred when we are able to look back, so trying to time cash into the market isn’t a great approach. By leveraging dollar-cost averaging, you smooth out your investment purchases and remove market timing.

Now is also a great time to consider a Roth IRA conversion. Roth conversions are a part of our normal consideration process for clients with IRAs, but they are particularly appealing when markets are in decline and your portfolio value may be lower. Conversions now may increase the likelihood of tax free growth as the market recovers. You may even be able to save on the tax bill you are paying now for that conversion due to the lower portfolio value. Less taxes and increased potential of tax free growth? That sounds like a great opportunity to be considering in a bear market.

A bear market also presents you with the opportunity to revisit your market risk tolerance. Are you feeling different now than how you felt when you originally discussed your risk tolerance with your Advisor? Perhaps you overestimated how much risk you could tolerate and need to evaluate dialing back market risk long term. The opposite could also be true. You may have always feared the worst and now, faced with a bear market, you aren’t as bothered as you thought you would be. These are valuable, real-time insights that can help you and your Advisor plan for the long term.

Above all else, remember that you are not alone. You are a part of the CapSouth family, and we value our long-term relationships with clients. We are here in the good times and in the bad. Do not hesitate to reach out to your Advisor at any time.

To discuss this article further or to learn more about CapSouth Wealth Management, visit our website at www.capsouthwm.com or call 800.929.1001 to schedule an appointment to speak with an advisor.

Investment advisory services are offered through CapSouth Partners, Inc, dba CapSouth Wealth Management, an independent registered Investment Advisory firm. Information provided by sources deemed to be reliable. CapSouth does not guarantee the accuracy or completeness of the information. CapSouth does not offer tax, accounting, or legal advice. Consult your tax or legal advisors for all issues that may have tax or legal consequences. This information has been prepared solely for informational purposes, is general in nature and is not intended as specific advice.

In what has been a limited but quite eventful career in finance, I frequently get asked by people how they should invest their money. As in most cases, there is no “one size fits all” answer to that question. The phrase “It depends” is used quite often in our company as many factors must be considered before making an investment decision. Warren Buffett might tell you to invest in a low-cost index fund and leave it alone for 30 years. Others may say that cash is king and to stick it under your mattress. Still, others may say to buy the newest Crypto-Token-NFT-Chain (I know that is not a real thing). The answer is rarely as simple as any of these options I mentioned, and I spend the majority of the day trying to answer what seems like a simple question, “How do I invest this money?” If you have paid attention to just about any type of media lately, you know that the stock market is not having its best run this year. With inflation at the highest level in 40 years and the Fed hiking interest rates three times already, and likely another next month, there does not seem to be a good answer to how to invest in these tumultuous times. Not since 1994 have we seen negative returns in both the stock and bond market, and cash is losing purchasing power due to the high inflation. So where do you hide? One such possibility is becoming more and more relevant and, fortunately, more available to investors. This is what the investment world calls Alternative Investments.

What are Alternative Investments

Alternative Investments are considered financial assets that do not fall into one of the conventional investment categories, such as common stocks, bonds, and cash. Sometimes called the private market, alternative investments cover many different categories such as private equity, private debt or credit, real estate or real assets, hedge funds, venture capital, futures, derivatives, and so forth. Alternative Investments (Alts) attempt to have the same outcome as public markets as they seek to generate return, provide growth, and protect assets while diversifying investments from the public market. Often, these investments have a low correlation to the public market allowing; many have less volatility than public markets and a lower risk profile in a portfolio. Until recently, Alternative Investments were only available to institutional investors and not the retail market. Regulatory changes and innovations in products and services have opened the world of Alts to a much broader market. In the past, retail and even high net worth investors had limited access to Alts due to high investment minimums, liquidity limitations, and accreditation requirements, however, a shift in focus has allowed a much larger number of investors to qualify and benefit from private investments. In many cases, investment minimums have declined, subscription processes have become more streamlined, and funds have even begun trading on the open market, albeit they are usually less liquid than your normal stocks or ETFs and may still have a hold period for liquidation. Investors are now able to differentiate their portfolios even further by using Alternative Investments as a standard in their investment process.

Why Invest in Private Markets

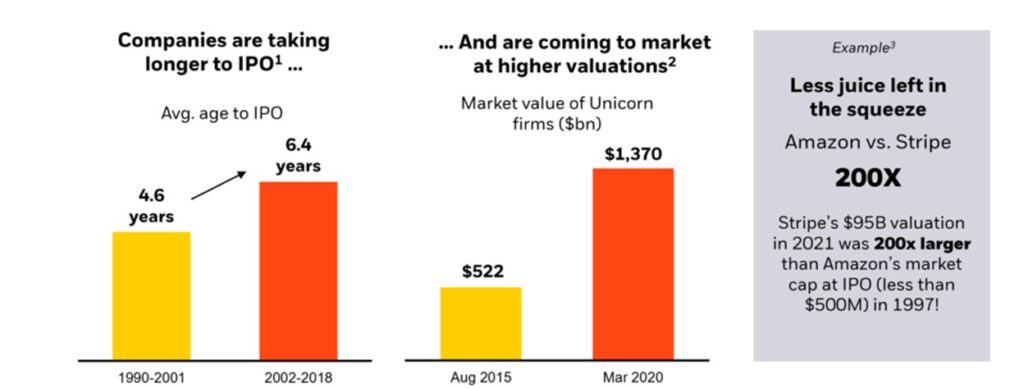

In current market conditions, it is now more important than ever to consider investing in private markets as valuations are fundamentally driven and not as impacted by market sentiment. In other words, news cycles, social media, and CEO popularity have much less impact on the companies’ valuations than those available in public markets. Through the use of private equity investments, companies are able to stay private much longer, without needing the investment from joining the public markets, and investors are able to benefit from a longer duration in the private market – kind of a chicken and egg situation. Much economic growth is now taking place in private markets as IPO’s are reaching the market at increasingly higher valuations, often leaving less potential for investment return once a company does go public.

Source: National Venture Capital Association. Data as of 12/31/19.

Source: Journal of Applied Corporate Finance. Private Equity and Public Companies. “The Growing Blessing of Unicorns: The Changing Nature of the Market for Privately Funded Companies.” Keith C. Brown and Kenneth W. Wiles, University of Texas at Austin. Sample set was determined as follows: The demographic and financial characteristics for sets of active unicorns at two different points in time: August 31, 2015 (the sample from our original study) and March 1, 2020. As before, to be included in either sample, a company must satisfy the following conditions: (1) have always been private; (2) have received at least one funding round of institutional capital; (3) not be a divisional buyout of a public company; and (4) have an estimated market valuation of $1 billion or more. Throughout the entirety of the surveying process, the identity of and data for these samples were gathered from several sources, including CB Insights, Capital IQ, CrunchBase, PitchBook, Preqin, and Wells Fargo, as well as their own research.

Large Private Equity funds generally hold a portfolio of companies, and successful fund managers purchase companies that have the potential to add value to the overall portfolio. In other words, they look to have the portfolio companies feed off each other, and, by extending their holding period, they are allowed adequate time to create value by implementing crossover initiatives. Investments in private debt and private credit focus more on providing a greater yield and overall return, than the public fixed income market while also maintaining and possibly increasing the value of their holdings. This is especially important at this point in time, as rising interest rates have historically caused a loss of value due to duration risk – something constantly discussed in investor meetings. Private real estate funds also focus on providing a yield, but with further potential advantages: growth opportunity due to property appreciation, tax advantages due to property depreciation, and the ability for real assets to hedge inflationary risks.

How Do Alternatives Deliver

When most people speak of investing, they are most familiar with one market, stocks listed on U.S. stock exchanges, which are public, liquid, and provide timely information to anyone who is interested. People rarely think about another, much larger market, the private market, where information is not as transparent and investments are generally not as liquid. For those unfamiliar with the investing term “liquid” (or liquidity), surprisingly, we are not discussing a favorite drink. Liquidity is referred to as how easily an asset can be converted to cash. Assets like stocks and bonds that trade on the public market can be converted to cash in a day or two. Alternative Investments are generally not as liquid, meaning you cannot just sell them over the counter and see your money quickly. There can be lock-up periods, partnership votes, property sales, long-term contracts, and many other protocols to convert an investment back into cash. Because of this lower liquidity, investors in private markets can demand a greater return on their investment, called a liquidity premium. Keep in mind that just because an investment is illiquid does not mean it guarantees positive returns or any return level; however, companies are generally willing to pay more for extended use of funds.

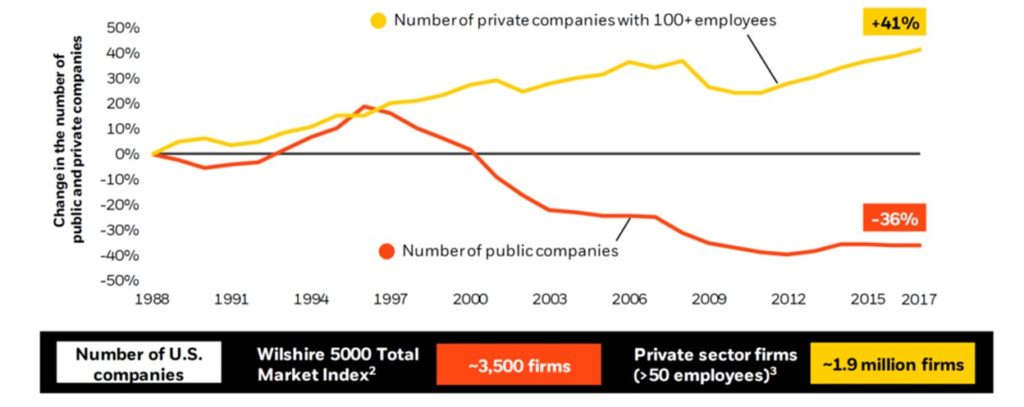

Going back to the overall size of the private market, we often think the public stock market composes the vast majority of the market. However, the private company universe is magnitudes larger than the public market. According to the US Census, there are approximately 6 million companies with employees in the U.S., only about 5,700 of which are listed on the New York Stock Exchange and the NASDAQ combined.1

1. Source: U.S. Census Bureau – Statistics of U.S. Businesses; Droidge, Karolyi and Stulz (1988-2017). Represents the latest data available as of 2/5/21.

2. Source: www.wilshire.com. As of 2/5/21.

3. Source: Kaiser Family Foundation, 2019 data; www.kff.org. Data updated as of 2/5/21.

Information, or lack thereof, is another driver of return for private investments. The SEC, or Securities and Exchange Commission, requires publicly listed companies to provide potential investors with annual reports and other disclosures containing information regarding their finances, strategies, and operating procedures. These rules theoretically allow all investors to be on the same playing field when evaluating an investment. Private companies are not required to provide investors with the same level of information and disclosures and, therefore, are more difficult to value, which in turn leads to the need for more educated investment decisions.

Are Private Investments Risky

Just like any other investment, or for that matter, any other decision we make in life, Alternative Investments pose certain risks. Interestingly enough, the same traits that make private investments valuable are also what make them risky. As discussed before, the lack of transparency in private markets, as opposed to public markets, leads to both risk and, hopefully, reward. Similarly, the liquidity premium you expect to be paid could also be detrimental if you were to have a need to redeem your investment in a timely manner. It is imperative to look at private investments over a long-term horizon and only invest funds that would not be needed in the near future. Some alternative investments also require investors to become partners in the fund, venture, property, etc., so it is essential for investors to understand the structure of the deal and confirm they are limited to loss of investment only and are not on the hook for further investment. Finally, alternatives can be highly concentrated, adding to a level of risk not generally found in ETFs, Mutual Funds, or market indexes.

In closing, Alternative Investments can be an impressive source of return, growth, and protection for many investors. Still, they should normally be considered a part of the overall portfolio, not the entire investment strategy. Anyone wanting to invest or learn more should read, research, and then speak to their tax, legal, and financial professionals about Alternative Investments before diving in head-first.

Investment advisory services are offered through CapSouth Partners, Inc, dba CapSouth Wealth Management, an independent registered Investment Advisory firm. Information provided by sources deemed to be reliable. CapSouth does not guarantee the accuracy or completeness of the information. CapSouth does not offer tax, accounting, or legal advice. Consult your tax or legal advisors for all issues that may have tax or legal consequences. This information has been prepared solely for informational purposes, is general in nature and is not intended as specific advice. Any performance data quoted represents past performance; past performance is no guarantee of future results.