Life Insurance as an Asset Class

By J. Scott Fain

July 2019

Viewing life insurance as an asset class provides an additional benefit to consider when evaluating the purchase or continuation of an insurance policy.

What do I mean by asset class? Traditional asset classes might include equities, fixed-income securities, cash equivalents, and real estate. These categories organize various financial tools into groups that have similar characteristics, primarily in terms of risk. Equities are generally considered to provide the greatest return over time, but also can carry the greatest amount of risk and volatility. Advisors and portfolio managers typically strive to diversify clients’ portfolios to manage the amount of risk taken while still achieving acceptable rates of return over time.

Through the types of investments referenced above, what circumstances are needed for you to make money? (Hint: We’ve mentioned two big factors twice already…) That’s right, you need returns and time. We all hope for long, prosperous lives, but what if death occurs prematurely? Now we have removed the element of time. Though our money may have been invested well, those investments may not have had time to perform.

So what options do we have available to provide a greater return in the short-run? You guessed it: Life Insurance. What if we had sufficient liquidity for our lifetime needs, and took one portion of our assets and invested in a life insurance policy? Let’s look at an example:

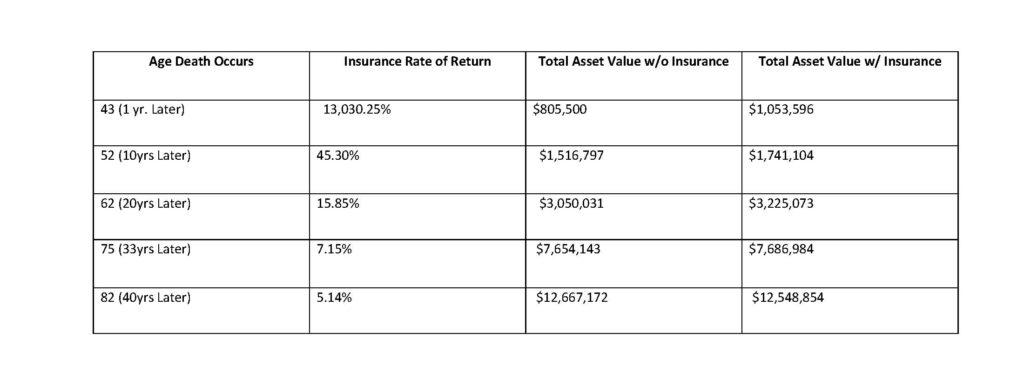

Charlie is a 42 year-old male in good health. Charlie is married to Sara, and they have two children, Larry and Mary. Charlie and Sara currently have $750,000 in assets, and Charlie has an annual income of $85,000. We will utilize sample average rates of return for the typical asset classes, and guaranteed internal rates of return for the life insurance death benefit based on a sample Nationwide illustration.

Charlie plans to contribute an additional $7,500 per year to his investments. Using a $1,904 annual premium for a $250,000 permanent life insurance policy guaranteed to Age 121, let’s look at potential outcomes:

Under this simplified example, if all typical investments average the assumed rates of return, the portfolio diversified with insurance is more favorable if death occurs any year through age 76. Following that age, investing the full $7,500 annually in equities would’ve generated a higher asset value. Note: These figures do not provide an adjustment for the tax savings. The $250,000 death benefit generated by the life insurance policy pays to Charlie’s heirs income tax free under current law. It is also important to note that the return generated by the life insurance policy is guaranteed, subject to the claims paying ability of the insurance company.

Might it be time for you to consider insurance as an asset class?

Contact CapSouth at 800.929.1001 for more information on this concept and how it might apply to your particular situation. Also visit our website at www.capsouthwm.com

CapSouth Partners, Inc., dba CapSouth Wealth Management, is an independent registered Investment Advisory firm. CapSouth does not offer tax, accounting or legal advice. Consult your tax or legal advisors for all issues that may have tax or legal consequences.